Despite a vast array of investment choices available today, Exchange-Traded Funds (ETFs) still stand out as one of the most flexible and cost-effective options. Whether you’re seeking long-term growth, steady income, or a hedge against inflation, there’s likely an ETF out there for it. Yet with literally hundreds of ETF categories now available, from broad market to niche thematic funds, knowing which one to choose can feel overwhelming at times. This article explores some of the main types of ETFs, how they work, and the pros and cons of each.

Broad Market ETFs

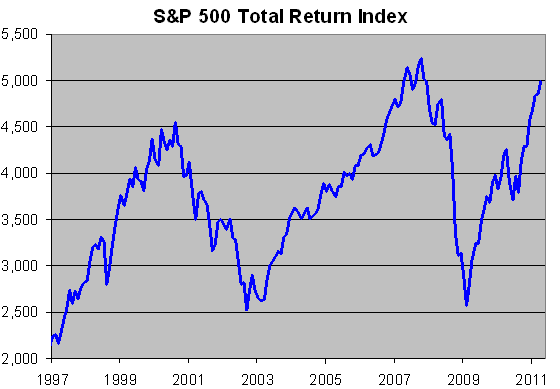

Broad market ETFs track a market index such as the S&P 500. They’re one of the most straightforward and cost effective ways to build a diversified investment portfolio. By tracking well-known indices they give investors instant exposure to hundreds or even thousands of companies across multiple sectors, and as they mirror an index rather than relying on active management they typically come with low fees. Broad market ETFs appeal to investors who want a “set-and-forget” approach, where long-term growth is achieved without the need to spend time picking individual stocks themselves. While these ETFs move with overall market conditions, and can therefore decline during downturns, their wide diversification helps smooth out volatility and makes them a strong core holding for many portfolios.

Key term:

Expense Ratio is the annual fee that investment funds (e.g. ETFs and mutual funds) charge to cover their operating costs. It’s expressed as a percentage of the amount invested. For example, if a fund has an expense ratio of 0.10%, that means the investor will pay $1 per year for every $1,000 invested. This fee is automatically deducted from the fund’s assets, so the investor doesn’t pay it directly. However, it does slightly reduce overall returns. Lower expense ratios are generally better for investors, especially over long periods, because even small percentage differences can compound into significant cost savings over time.

Pros

- Automatic diversification: Investing in a single broad market ETF can give exposure to hundreds or even thousands of companies.

- Low cost: These funds typically have some of the lowest expense ratios in the industry.

- Long-term growth potential: Broad market indices have historically trended upward over long periods of time.

Cons:

- No extra performance: These ETFs follow the market, they don’t try to beat it.

- Exposure to downturns: When the entire market drops, broad market ETFs can automatically drop with it as there is no manager to step in.

- Dividends may be modest: As they include a mix of growth and value companies, the income generated from dividends can be lower than that of dividend-focused ETFs.

Sector ETFs

Sector ETFs allow investment in specific areas of the economy such as technology, energy, or financials, rather than the broader market as a whole. By targeting a specific sector, these ETFs can make it easier to capitalize on growth trends and industry-specific opportunities without the need to spend time researching and picking individual stocks. For example, a technology sector ETF might benefit during periods of innovation and strong corporate earnings in the tech sector, and a consumer discretionary sector ETF could benefit during periods of economic expansion, when consumers have more disposable income to spend. However, because sector ETFs are less diversified than broad market funds, they tend to be more volatile and can decline sharply if problems emerge in that particular area of the economy. This concentration risk means sector ETFs are best used to complement a diversified portfolio, rather than as a standalone core investment.

Key term:

Consumer discretionary refers to goods and services that people choose to spend money on after their basic needs are met. These are non-essential items that consumers typically buy more of when the economy is strong and they have higher disposable incomes, and cut back on during economic downturns. Examples include cars, entertainment, and travel.

Pros

- Investment focus: Allows investors to tilt their portfolio toward specific areas of the economy they believe will outperform.

- Personal vision: Investors can align investments with their personal views on economic cycles or emerging trends.

- Growth potential: If a particular sector experiences strong earnings growth, technological breakthroughs, or favorable economic conditions, a sector ETF can outperform a broad market ETF during such periods.

Cons

- Higher volatility: As their performance depends heavily on the fortunes of one part of the economy, sector ETFs can experience strong gains but also deeper losses.

- Concentration risk: Investing heavily in one sector of the economy increases downside risk if that sector faces challenges. For example, the Dot-Com Crash of 2000 wiped-out much of the value of tech stocks at the time.

- Requires research: As investments are being increased in a particular sector, more research and attention is required than with broad market ETFs.

Bond ETFs

Bond ETFs are investment funds that hold a diversified portfolio of bonds and trade on exchanges throughout the trading day at market prices like stocks. This is distinctive compared to traditional bonds which may trade infrequently. Bond ETFs provide investors with exposure to different types of bonds without investors needing to buy them individually. Bond ETFs can be composed of government, corporate, municipal, and even international bonds issued by foreign governments and corporations, allowing investors to diversify globally without buying individual foreign bonds themselves which can be complex due to currency, legal, and market differences.

Key term:

Coupon payments: When investors buy a bond, they’re essentially lending money to a government or corporation. In return, the issuer promises to pay interest (called a coupon) at fixed intervals until the bond matures. These periodic interest payments are called “coupon payments” because in the past investors literally clipped coupons from paper bonds to redeem the interest. At maturity, the investor receives back the “principal” which is the face value of the bond.

Pros

- Income: Bond ETFs collect the coupon payments from the bonds in the fund and typically distribute these to investors as regular payments (monthly, quarterly, or semiannually, depending on the fund).

- Diversification: By pooling multiple bonds into a single fund, bond ETFs reduce the risk associated with any one issuer.

- Professional management: Bond ETFs benefit from professional management as the ETF provider handles bond selection and the management of coupon income, simplifying the process for investors.

Cons

- Interest-rate sensitivity: Bond prices fall when central banks raise interest rates. This is because newly issued bonds pay a higher coupon based on the new higher interest rate, making older bonds paying a coupon based on the previously lower interest rate less attractive.

- Income is not guaranteed: Income payments can fluctuate depending on changes to interest rates made by central banks, or credit events (such as defaults) within the underlying bonds.

- Lower returns: Bonds typically offer lower long-term returns than stocks. Historically, stocks have delivered roughly 9–10% per year versus 5–6% for bonds in U.S. markets (based on long-term averages).

Dividend ETFs

Dividend ETFs invest in companies known for paying dividends. Their focus on companies that regularly pay out a portion of their profits to shareholders makes them an attractive choice for investors seeking a steady stream of income. These funds typically hold a diversified basket of dividend-paying stocks which are often mature, financially strong businesses with consistent cash flows.

Pros

- Income: The ETF provider collects the dividends paid out by the companies in the fund, and then (after subtracting fees/expenses) distribute these dividends to the ETF’s shareholders, typically on a monthly, quarterly, or sometimes annual basis.

- Spreads the risk of dividend cuts: Even if one company reduces or suspends paying out dividends, the ETF structure cushions the impact of this because dividends come from many companies.

- Lower volatility: Companies that pay dividends are usually more stable because these companies tend to be more mature and established. They often have long operating histories, relatively predictable revenue streams, and strong market positions. This is in contrast to start-ups and early stage companies which typically need to re-invest profits rather than paying them out to shareholders.

Cons

- Lower Growth Potential: Companies which pay out dividends often reinvest less into expansion. This can result in dividend ETFs growing slower than funds which are focused on high-growth stocks, and may miss out on the explosive upside of some of the newest and most innovative companies.

- Dividends are not guaranteed: During a widespread economic downturn or financial crisis, even stable companies can reduce their dividends or suspend them altogether, causing income from the ETF to drop.

- Higher Fees: Dividend ETFs often have higher fees compared to broad market ETFs due to screening and selection criteria.

Thematic ETFs

Thematic ETFs focus on specific long-term trends and investment themes such as renewable energy, artificial intelligence, space exploration, cybersecurity, and electric vehicles. These funds allow investors to gain targeted exposure to innovative and fast-evolving areas of the economy they believe will shape the future.

Pros

- Access to emerging industries: They provide a simplified way to invest in complex or cutting-edge areas of the economy without deep technical knowledge.

- Engaging: Investors can align their portfolios with their own interests and beliefs.

- High upside potential: Rapidly growing industries can potentially produce significant gains.

Cons

- Increased volatility: Emerging technologies and less established companies can rise and fall quickly.

- Uncertain future: Not all trends necessarily materialize into profitable industries, and their long-term success can not be guaranteed.

- Higher expense ratios: Many thematic ETFs have higher expense ratios than broad market ETFs because they often require more active management including research, screening of included companies, and frequent re-balancing of the included companies to ensure the fund remains aligned with its stated theme.

Commodity ETFs

Commodity ETFs track assets such as gold, silver, oil, and even agricultural products like wheat or coffee. They provide investors with exposure to commodities without the need to physically buy or store the underlying assets themselves. These ETFs typically track commodity prices either by holding the physical commodity itself (as is common with precious metals) or by using futures contracts.

Pros

- Diversification: Commodity markets often have a low or inconsistent correlation with stock markets.

- Inflation hedge: Commodity prices often rise when inflation is high.

- Lower barriers to entry: Investors can gain access to commodities with relatively small amounts of capital, unlike direct commodity investing which can be capital-intensive.

Cons

- High volatility: Even though they may move independently of stock markets, commodity prices can still swing dramatically.

- Unpredictable market drivers: Shifts in supply and demand, geopolitics, and weather events can all impact commodity prices.

- No dividends: Most commodities don’t produce income.

ESG ETFs

ESG (Environmental, Social, and Governance) ETFs are designed for investors who want their portfolios to align with sustainability, ethical considerations, and responsible corporate behavior. These funds invest in companies that score well on factors such as environmental impact, social responsibility (including worker relations and diversity), and strong corporate governance. ESG ETFs allow investors to pursue long-term growth while supporting businesses that prioritize issues like environmental impact and fair treatment of employees. They often track broad or sector-based indices with additional screening criteria, providing diversification alongside values-based investing.

Pros

- Sustainability-focused investing: Allows investors to align their portfolios with their personal beliefs.

- Diversification: Many ESG ETFs include hundreds or even thousands of companies across multiple sectors.

- Potential for growing demand: ESG-focused companies may benefit as sustainability becomes an ever-growing concern.

Cons

- Definition differences: ESG definitions and methodologies can vary between providers.

- Higher expense ratios: ESG screening of companies can increase costs.

- Potentially reduced universe and performance: Screening may exclude high-performing companies that do not meet the ESG criteria.

International and Emerging Market ETFs

International and emerging market ETFs allow investors a relatively straightforward way to invest in companies located in different countries around the world. This can including those in developed economies like Europe or Japan, and faster-growing emerging markets like India.

Pros

- Growth opportunities: Provides investors with access to growth opportunities in other parts of the world. Some emerging markets can deliver strong returns due to factors such as rapid economic expansion, infrastructure development, growing middle-class populations, and increasing consumer demand.

- Global diversification: Helps diversify portfolios geographically beyond U.S. markets.

- Currency benefits: If the U.S. dollar weakens, this can boost international and emerging market ETFs, as foreign assets become more valuable in dollar terms.

Cons

- Geopolitical risk: Some emerging markets can experience political or economic instability, and this instability can negatively affect returns.

- Currency fluctuations: Shifts in currency exchange rates can be unpredictable.

- Transparency risk: In some emerging markets, the underlying companies may not always provide complete or timely financial information due to weaker reporting standards, less rigorous regulatory oversight, or opaque corporate practices. This transparency risk can lead to inaccurate company valuations.

Conclusion

Since their first introduction in the early 1990s, there is now a wide range of ETFs available for investors to choose from. Due to the emergence of this enormous variety, it’s now possible for investors to mix various types of ETFs together to create an investment portfolio bespoke to their views, goals, risk tolerance, and timeline. For example, it’s now possible to construct a portfolio in which dividend and bond ETFs provide income, sector and thematic ETFs add targeted growth opportunities, commodity ETFs provide diversification and help hedge against inflation, all while international ETFs expand global reach. By blending different types of ETFs thoughtfully, investors can build their own unique portfolio which is aligned with their individual interests and investment objectives.

Disclaimer: The purpose of this website is education and financial journalism. It is not a recommendation or personalized financial advice. Your personal circumstances have not been taken into account, and this website is not a substitute for consulting a qualified financial advisor. All images are for illustrative purposes only. Past performance is not indicative of future returns.